How to make $1 million with your military pay

SUMMARY

Getting your first paycheck on active duty is awesome — because getting paid is the best. But most of us don't know what to do with that money. Buy a Camaro? Stuff it in a mattress? Maybe...but what about turning it into a million dollars?

It might sound too good to be true, but it actually isn't. Let's talk about a simple financial product for beginning investors: the Roth IRA.

First: Some good news for service members. America's new tax plan combined with a military pay raise is giving troops a nice little bump in their wallets.

Pay grades E-1 to E-6 are now in a new, lower Federal tax bracket.

This could be add up to 00 a year in savings — and that's before you start making those deductions, so your newfound wealth might even be higher.

PLUS you got a pay raise of up to 00 so that's an extra two grand a year right off the bat. Baller.

But before that wad of cash burns a hole in your pocket, consider the smart way to spend this money – money you won't even miss. The Roth IRA is one easy way to do it — and it could make you a millionaire.

You can take that post-tax income and make non-taxable money while you sleep. This is literally the least you can do for retirement -- and again, it's super easy.

With a Roth IRA, you contribute to an individual retirement account (IRA) after taxes (meaning there is no tax benefit) BUT you are not taxed when you withdraw the funds. And those funds are going to growwwwww.

That's an investment of 8.33 per month.

So if you max out your Roth IRA from age 18 to 65, you'll be taxed against the 0,000 you invest...but you'll retire with id="listicle-2626415708".5 million that you can withdraw tax-free.

Here's how it works.

The Roth IRA is an account that holds your investments — you can select the investment options and risk strategies yourself or seek advice from the brokerage entity you're investing with.

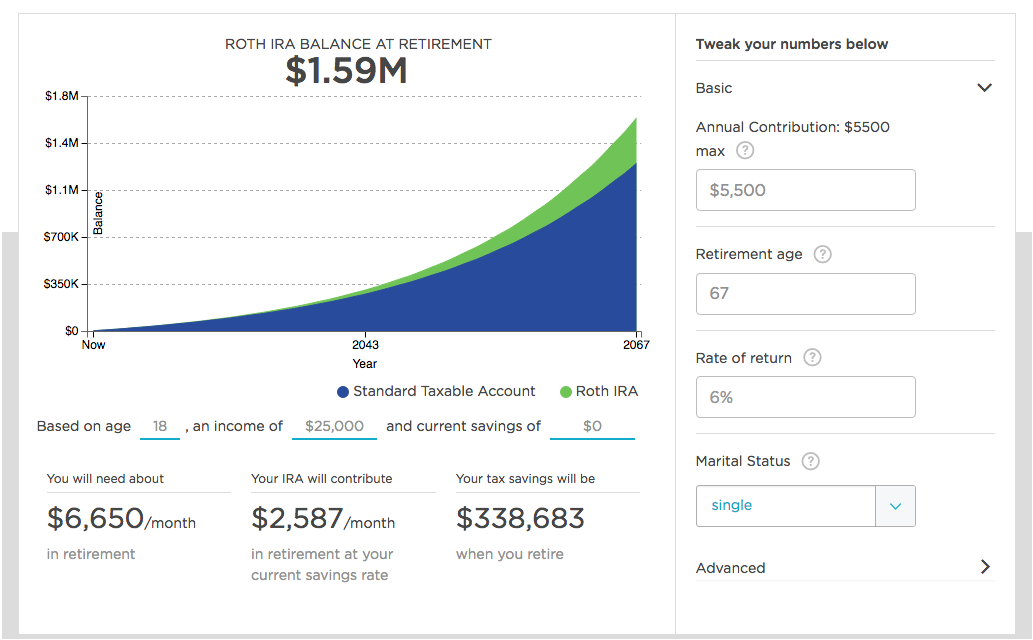

Each year, you can max out the yearly contributions the government allows, which in 2018 is ,500 (It's ,500 if you're over the age of 50, but for now, we're just going to do the math for the fifty-five hundred dollar bracket).

So you select your investment options, probably with higher risk if you're younger, and set up an automatic contribution of 8 per month.

Do this from age 18 to 65….

...with a decent compounded interest rate of… say …. 6 percent (the market actually did 8.3 percent in the last ten years but just to be safe...)

...and you will make 1.59 million dollars over your lifetime.

The most important thing to remember when investing is compound interest.

Investing consistently over time means you are increasing the amount invested AND earning interest on what you've invested AND earning interest on your interest.

This is why it's critical to start early and be consistent. Even a small amount invested over time can yield greater results than a large amount invested later with no time to grow.

So if you're getting a later start, don't panic. If you begin at age 30 and max out your Roth IRA until age 65, you can still end up with 0,000 at retirement — and again, that's just with a 6% rate of return, which is a conservative estimate based on lower-risk options.

The bottom line is to start as early as you can and be disciplined about it.

Spending 8 per month to max out your Roth IRA might seem like a lot when you're an E-1 earning about 00 a month — but remember, that income is discretionary. The military has benefits like BAH and health insurance — it's got the big stuff covered, so be wise with how you budget the rest of your income.

And again, if you set up automatic payments, you won't even miss that money.

I know you want to buy video games and an 80-inch big screen for the barracks...but resist that urge and set yourself up to be a ballin' millionaire later.

SHARE