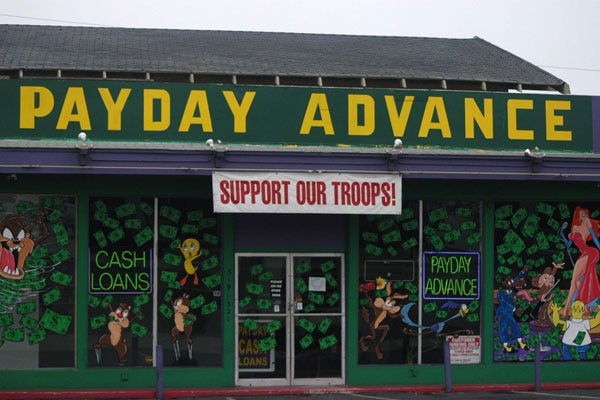

The American Forces Press Service reports that payday loans have become a $40 billion business and are especially prominent outside military bases. David VanBeekum, a market manager for a local bank near Hill Air Force Base helps to educate Airmen about how payday loans work. He said Utah has 350 payday lenders and almost 10 percent of them are located just outside the base’s gates.

But you don’t have to physically go to the stores. The Internet has 2.5 million links for payday loans, 4 million for cash advance sites; and 31 million for check advance sites. In addition, the Hill Air Force Base Airman and Family Readiness Center, which offers financial counseling services for military members, found that in California the payday loan outlets outnumber McDonalds and Burger King restaurants combined.

Typically, payday loans are for relatively small amounts of money in increments of $100, up to $1,000. It’s easy to obtain one of these loans. All anyone needs is a bank account, proof of a steady income such as a pay statement, and a simple form of identification. It takes about 20 minutes to secure a loan.

Payday lenders target women, those who earn $25,000 or less per year, minorities, and military members. The borrower writes a personal check or grants electronic access for the amount of the loan and a finance charge. However, these loans are not long term and become due on the borrower’s next payday, either in one or two weeks. The interest compounds quickly and calculates to an average of 390 to 780 percent annual percentage rate. There’s no payback installment plan so the borrower must pay the entire amount due in order to avoid another finance charge associated with an extension of the entire loan principle.

This style of business traps the borrower into a repetitive cycle. On average, a person choosing a payday lender ends up with eight to 12 loans per year. A successful payback of the loan is not reported to the credit bureaus and there are documented cases of companies resorting to unlawful or questionable collection tactics.

Each state establishes its own regulations, finance fees and interest rate limits, not the federal government, Mr. VanBeekum said. There’s even a lender in Utah who charges as much 1,335 percent, and even though they’re required by law to advertise the interest rate, 75 percent of them do not.

The Consumer Federation of America, a non-profit advocacy group, has studied the payday loan industry for the past 10 years and said the industry meets the criteria for predatory lenders who have abusive collection practices, balloon payments with unrealistic repayment terms, equity stripping associated with repeated refinancing and excessive fees, and excessive interest rates that may involve steering a borrower to a higher-cost loan.

Besides the high interest rates, CFA surveyors found they misrepresent themselves as check cashers even though they are not registered with the state as a check cashing entity. They will not cash your personal check. Instead, they are only willing to hold your check until payday. The lenders will threaten or badger the client into paying the loan and many people end up rolling over the entire balance of the loan, and thus incur the finance fees again. A number of payday lenders have also ignored the Electronic Fund Transfer Act and found ways to access a consumer’s account when not authorized or when authorization was withdrawn.

The PenFed Foundation’s Asset Recovery Kit (ARK) provides a no-interest alternative to predatory lending for active duty, reserve, and National Guard military.

Fees for predatory payday loans can be an astronomical $19 for each $100 borrowed until payday. Through ARK, one can borrow up to $500 with a flat fee of $5 and no interest for one month.

ARK is a hassle-free, confidential, and smart way to deal with money problems.

- Active duty, reserve, and National Guard military are eligible

- No credit report is pulled because those with emergency cash needs have already exhausted their options.

- No interest is charged, just an application fee of $5. With ARK, you don’t fall further into debt.

- Immediate cash loans up to $500 (or 80 percent of net pay) are available for one month.

- There’s minimal paperwork just a simple one-page form.

- It’s completely confidential, meaning we don’t tell anyone who has come to see us.

- Up to three loans in six months are available, but after the first ARK loan, the recipient must sit down with a local Consumer Credit Counselor identified by the foundation.

ARK was designed to be as easy as a payday loan, but without the negative consequences. The goal is to rebuild or repair credit, improve cash flow and increase money-management skills.

PenFed partners with credit unions across the country to bring the ARK program to military men and women. They welcome new credit union partners. Please contact them to learn more.