Here’s why millennial veterans home ownership is on the rise

SUMMARY

Many millennials and members of generation Z are putting off buying a home. It's not hard to blame them for that. Housing prices have gone up, and it is a lot harder to save for that big down payment when purchasing your first home. Home purchasing among millennials has dropped with the exception of one demographic: veterans.

There has been an eight-year increase in veterans using the VA home loan, up 43 percent. In 2019 alone, there were 624,000 loans backed by the VA, and a majority of these loans were held by millennials.

That number will go up even more in 2020 thanks to a change in benefits.

A new law signed by President Trump this past June, the Blue Water Vietnam Veterans Act of 2019, makes it even easier for veterans to move into the home of their dreams. The part of the law that affects homebuyers was the limit on how much veterans could borrow without a down payment.

There is no longer a limit on how much a veteran can borrow. If you qualify, you can now take out a bigger loan with no down payment.

The VA home loan is a wonderful resource for qualified veterans. VA loans are mortgage options issued by private lenders with zero down and backed by the VA. The loans can only be used for primary residences, not properties used for investment. However, they can be used to refinance an existing mortgage.

With housing prices soaring in certain parts of the country, there was a major roadblock to the VA home loan. The loan would only cover the value of the house up to a certain amount. As a result, if a veteran wanted to use the VA home loan to purchase a house that was more to their needs and desires and it was over the limit, they had to front a portion of the extra amount as a down payment.

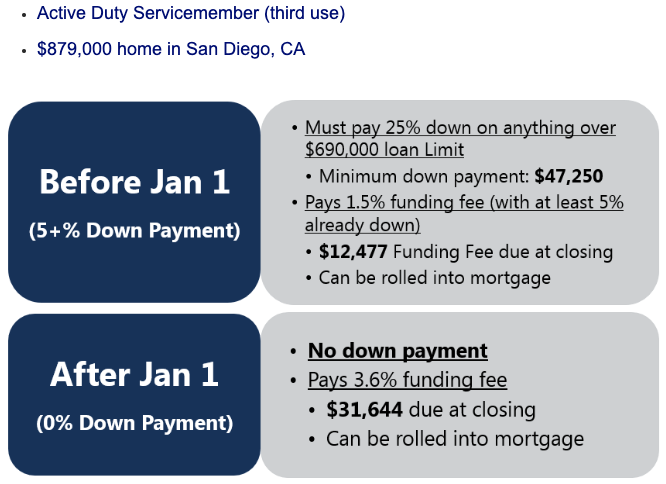

Jeff Jabbora is a Marine veteran who has spent the last seven years as a real estate agent in San Diego County. When asked about the new law, he said the new law "enables qualified veterans, who qualify for a loan amount over the local area maximum to be able to not have to put money down on the loan. For example, if the local/county loan limit for where the veteran is buying the home was 0k, and the veteran was buying a 0k property, with the previous program, the veteran buyer would need to bring money to the table on the overage. Most often, 25 percent. So in that scenario, it would be 25 percent of the overage of, 0k, which would be k."

Before the law went into effect, the limit dissuaded veterans from moving into houses that were more suitable for them and limited their housing options. This was most noticed in areas like California, the D.C. area, the Northeast and cities with high housing costs. According to data from Realtor.com, a whopping 124 U.S. counties had a higher average list price than the 2019 loan limits. When you compare the cities with the highest median housing cost versus the cities where veterans use their VA home loan, you see that 50 percent of those cities are similar.

Veterans in Los Angeles will see the biggest savings. The average listing price in L.A. is id="listicle-2645370998",655,468. Based on that number, VA borrowers would have had to come up with a down payment of 2,236. Now they don't have to.

Here is an example of how it works.

With the new law in effect, there should be a marked increase in homeownership among veterans.

As with the VA home loan, steady and suitable income as well as credit comes into play.

Owning a home is a point of pride..thanks to this new law, more veterans can have the opportunity.

SHARE